Eric Affeldt, President and CEO, ClubCorp

“And my business is doing quite well, thank you,” said Eric Affeldt, President and CEO of ClubCorp, in an interview with C&RB shortly after the management firm announced its acquisition of Sequoia Golf.

After going public last year and acquiring Sequoia Golf at the end of this summer, ClubCorp continues to raise its profile as a prominent face of the club industry. For insights on where the management firm sees its business, and the industry, going next, C&RB President Dan Ramella and Editor Joe Barks recently sat down with the face of ClubCorp, President and CEO Eric Affeldt, in his Dallas office:

C&RB Will your acquisition of Sequoia change perceptions about the state of the golf business?

Affeldt By default, given our public status, I’ve kind of become the spokesperson who’s going around talking to the investment industry and saying, wait a minute—I’m sorry that Dick’s [Sporting Goods] had a bad quarter [that was blamed in large part on golf], but my business is doing quite well, thank you.

But it is a fact that our business is less about “Golf” now, with a capital G, than with a normal g. The Baltusrols, Pine Valleys and Augusta Nationals will continue to do great—but they’re a very small part of the market.

We have to appeal to the broadest segment of society possible—and while one of the things we have [as part of that appeal] is golf, we also have tennis, fitness, swimming, social [activities], and contemporary dining facilities.

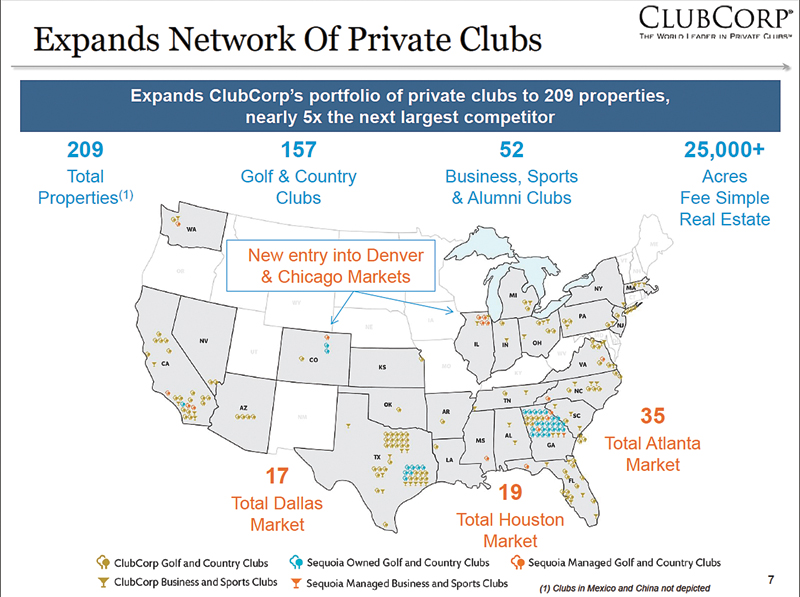

After its acquisition of Sequoia Golf, the ClubCorp portfolio reflected increased density in the Atlanta and Houston markets and new entries into the Chicago and Denver markets.

I want people, as they look around for their options for recreation, to say, my goodness, why wouldn’t I be a member of ClubCorp? With Sequoia, we’ll be over 200 total clubs, and we’ll have affiliate relationships with over 700 other resorts, hotels, restaurants, etc. I want people to say, I want that, because they offer me so much more than just a single club, or just golf.

C&RB Have you seen membership ranks continue to grow at your properties?

Affeldt Last year was our best sales year for new memberships than in the preceding 10 years. And this year we’re ahead of that pace, not even counting the new members from Sequoia [clubs].

Analysts say, aren’t you concerned that golf rounds have declined steadily over last decade? The fact is, our [annual] rounds per member haven’t moved out of a range of 53 to 57 for over 10 years. Through the recession, pre-recession, post-recession, it hasn’t budged. The fact that overall rounds in the industry have declined again, a lot of that is coming out of daily-fee golf, which is the space that got hurt the hardest in the downturn.

But again, rounds are secondary; my business is dues. I tell everybody we’re not in the golf business, although our golf and country club division makes up 85% of our total profitability. We’re in the membership business. So I really track, religiously, net dues, which is bodies in, bodies out, upgrades/downgrades. That’s the Holy Grail and by that measure, we are again pacing back up to pre-recessionary levels—we’re above it in golf/country clubs, and we’re playing catch-up in our business club division.

C&RB Can you speak to food and beverage and how important it is now to clubs, particularly in the context of the “reinvention” improvements you’ve made at many of your properties?

Affeldt It’s very important. F&B is our second largest revenue center, after dues; we do about $220 million in F&B revenue, out of $850 million [total]. Half of that revenue on the F&B side is private events—banquets, weddings, outings.

Las Colinas Country Club in Irving, Texas is one of many ClubCorp properties that have undergone dramatic “reinventions.”

C&RB Is that the ratio you’d like to see? Many see 60-40 as an ideal mix.

Affeldt We don’t—coming back to what I said before, we’re in the membership business. At some of our business clubs—the top-of-tower, downtown dining facilities—one of the things members have grumbled about, and rightfully so, is you guys are doing [an event] every night, I can’t even get into my club, why am I paying you dues? So we’ve literally had to take space and say this is dedicated member space—it may not be the whole club, but rest assured you will have your space in your club when you want to use it. So you have to walk a fine line in that area.

C&RB While dues is still the biggest revenue category, is F&B the fastest-growing category?

Affeldt It is, for a couple of reasons. One is the response we get from the reinventions. At some clubs where we’ve spent $2 million on improvements, in the first year we saw a 70% increase in a la carte cover counts. At that point, I thought, OK it’s new, it’s interesting, but like all of us, people will give a restaurant a try and then go to the next new restaurant. But in the second year, we increased 40% over the 70%; we paid for the [improvements] in two years.

We also made a change to something the company started in 1999, called Signature Gold, which was an add-on to existing dues that allowed you to travel around and use other clubs in the network. But if you didn’t travel, you saw no benefit in the product. So the [percentage] of members taking the deal stayed in the low 30s from the time we [KSL Capital Partners] bought [ClubCorp, in 2006].

Then we said, what if we created a really compelling home-club benefit, too, so now the person who doesn’t travel says hmm, I might be willing to pay more dues if I could get that. And we put the two together into the O-N-E membership: Optimal Network Experience. Now you not only get the traveling benefits all around the country, we give you 50% off your home-club food, for you and your family.

We’re now up to 44% of our total members taking this product, and the incremental usage of the club [makes up for] the reduced margins on the food. Remember, dues is the most profitable thing we sell. And we’ve also seen this wonderful phenomenon where you go in with your wife and say, honey, we just ordered two steaks, they used to be $20 apiece, they’re now $10 apiece—so I’m going to order a nicer bottle of wine.

The discount is only for food, not beverages, so we get the benefit of selling up what’s already a higher-margin product.

Business, sports and alumni clubs, such as The Columbia Tower Club in Seattle (left), comprise about a quarter of ClubCorp’s portfolio.

C&RB How are you trying to distinguish “the ClubCorp approach” from a service standpoint?

Affeldt Through something we say in almost all of our material: Building Relationships and Enriching Lives. When I go around and talk to our teams in the field, I ask our employee partners, what do you do?

And if I get answers like I sell memberships, I’m a chef, I’m on the maintenance team, I’m a golf pro, I say that’s interesting—but I really hoped you’d say, I happen to be a chef or a membership director, but my mission every day is to help build a relationship and enrich a life. And if I ask you to describe a good day, it’s not “I sold five memberships”; it’s “I helped a member with his daughter’s event that was coming up, and they were so happy.” Because by virtue of focusing on helping other people, either in their relationships or just having fun, you’re going to sell memberships.

Another example comes from after we bought the company. One of the things I mandated was that every Saturday morning at every single golf club, we would have a pro walking back and forth on the driving range, giving free lessons.

I got e-mails from golf pros saying, you’re taking money out of my pocket. My response was, Are you kidding me? A) nobody else is doing it, so you’re going to differentiate your club from all the other competitors, B) your guest, who’s out there playing with you, is going to go, Holy Cow, what was that all about—oh, it’s just something we do at the club every weekend, they come around and give tips. And lastly, if you fix my hellacious slice, where do you think I’m going for the rest of my life for my lessons? But the tunnel vision of, I get paid to instruct golf, as opposed to, I get paid to build relationships and enrich lives, is something we’re always working to eliminate.

C&RB Do you still fight the perception that you’re “too corporate,” especially with clubs you’re absorbing?

Affeldt Less so, because we’ve worked hard to convey an attitude of not being rigid or bureaucratic, and on focusing to all work together to try to make a place better. But having said that, in talking to investors and analysts over the last year, when I’m asked what our greatest challenge is, I still have to say people. This is a high-touch business. And as much as you and I get that and say, gee, how hard could it be, some of our people are still like, I don’t want to disturb members or try anything too different..

We’ve really tried to emphasize the personal nature of an individual club. When we have our GM schools, I’ll ask the room of GMs, I’m driving into your club, what do I see? Some of the newer GMs who’ve come into the company will say, landscaping, the fence. But someone like Lisa Neel, the GM here in Dallas at Brookhaven Country Club, has been with us long enough that she’s immediately going to say, “Lisa’s club.” And that’s the right answer. It’s not Brookhaven, it’s Lisa’s club. Everything that is happening in that club is happening because she has set the direction and has told people this is my expectation for how this club’s going to work.

C&RB As you grow, and particularly as you build up some large clusters in certain markets, will reinvention still be a club-by- club thing, or does it become a market-by-market thing?

Affeldt That’s an interesting question, and it’s particulary interesting as it relates to the Sequoia acquisition. Because they are so dense in Atlanta. They have two products—one, under the Canongate brand, is very golf-centric, with no tennis, no pools, and only one has a significant banquet facility. So with that cluster we’ll probably wind up picking a club or two and really making them full-blown, fully amenitized clubs, and let the members rotate around and use it. We don’t think we’d have to do it at every single club.

Then for [the Sequoia clubs] in north Atlanta, which are more traditional [and more in line with] our model, we’ll probably wind up going club by club and making improvements there.

I will also say this, to [Sequoia Golf President and CEO Joe Guerra’s] credit: we tend to buy clubs that are either undermanaged or undercapitalized, [but] Joe’s clubs have been extremely well-managed. That’s not the issue. And they’ve been well-capitalized in terms of maintenance [capital expenditures], but their current owners have not been willing to put the incremental dollars into the clubs to do the reinventions.

C&RB Is Sequoia indicative of the type of deals you’ll likely do going forward, or will individual clubs that you find and like come into the mix as well?

Affeldt I get the question repeatedly, where do you find clubs to buy, and who are your sellers? Relative to the latter, the seller universe consists of a few people who I would describe as ‘unnatural’ owners—a bank or insurance company or other institution that took back a facility or that owns a facility in a portfolio, but it’s not really their core business. Or a real estate developer that [as part of] building homes, amenitizes the community and then sells out. You have Toll Bros. that’s established its own [club] division, but Pulte [Homes], Shea [Properties], they’re really unnatural owners.

The other bucket of owners would be equity clubs. And interestingly enough, while some people say that constitutes the majority of the private club market in the U.S. and they’re not going to sell, six out of 10 of our last individual course deals were equity clubs.

Another seller bucket would be [an individual] who decides gee, I’ve got an affinity for golf, I want to own a golf club. And it may work and it may not work. And the last group would be the professional management companies, a la Sequoia. And this is where it’s interesting. If at the beginning of the year you looked at the landscape and said OK, who are the largest owners and operators in the industry—Troon, ClubCorp, American Golf, Billy Casper, Century, Sequoia—the majority of those were owned by private-equity firms. If you know anything about private equity, you know that they recycle capital; they buy companies and they sell companies. And if you then went and really did your homework, and looked at how long those portfolio companies had been in private-equity hands, you would see that all of them have been held by the private-equity owners for longer than seven years, when the typical holding time period is going to be five to seven years. So you would logically go, hmmm, I bet some of these things are going to trade. And lo and behold, American Golf trades, Troon trades, Sequoia trades.

So we will continue to do one-offs, and the odds of doing another portfolio company is much smaller.

C&RB Is there a preference to acquire, as much as there might be to just take over management responsibilities?

Affeldt Even more so since we bought Sequoia, I’ve said that I’m much more interested in ownership than in management, because of the difference in the economics. If we average 28-29% operating margins in our golf and country clubs, which we do, I’d much rather make that percentage off of whatever the revenues are than 3% in reimbursibles. The economics are radically different. And [ownership] has provided us with the ability to put $400 million-plus back into our clubs in the last seven years. No management company comes close to that. Which is why I had members in the recession saying, thank you, my neighbor’s club is [suffering], and you guys are spending a couple of million bucks on our clubhouse.

Tell Us What You Think!

You must be logged in to post a comment.